Crosswinds to Opportunities:

Navigating the Business Landscape in 2026

By AMCHAM T&T Staff Writer

You can view the complete set of presentation slides on our website,

https://s3.us-east-1.wasabisys.com/amchamtt-documents/AMCHAM Economic Outlook Forum 2026 FINAL.pdf

A Cautious but Pragmatic Outlook

Key results

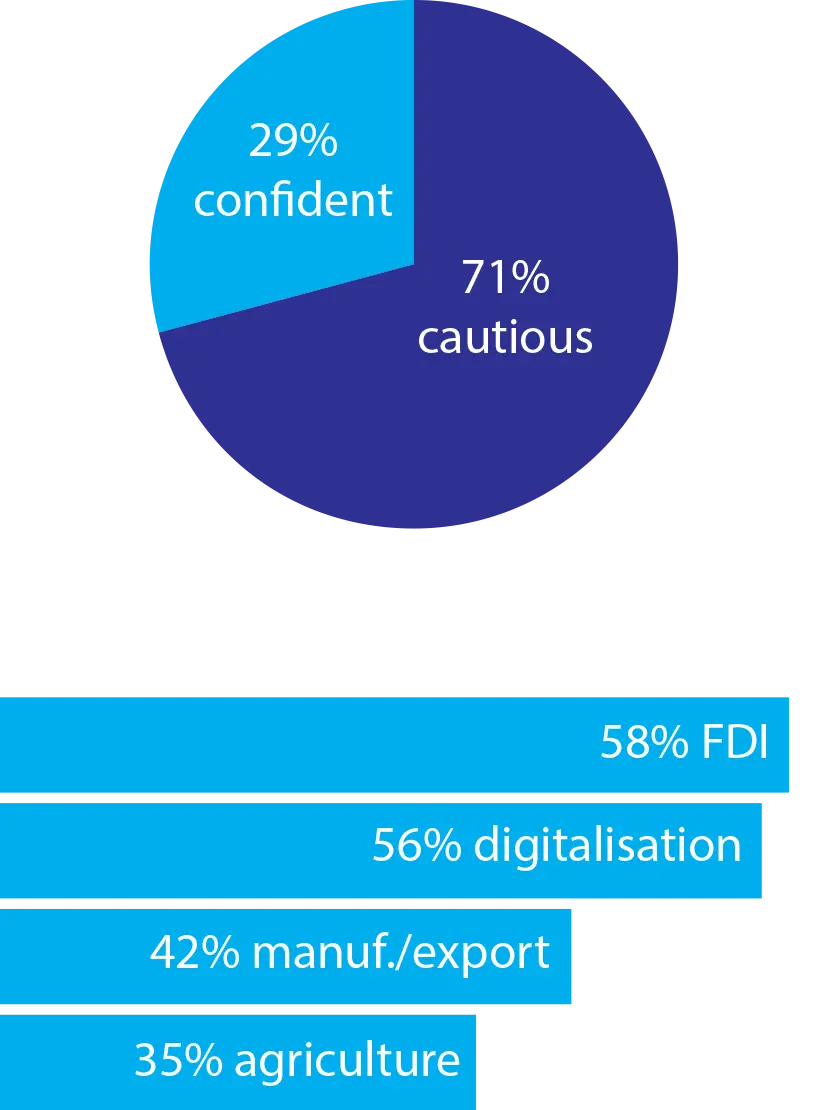

Businesses are entering 2026 with measured expectations. While 29% of respondents express confidence in the economy, the majority (71%) remain cautious. This represents an improvement from 2025 (21%), but confidence is still well below levels seen in earlier years.

That caution is grounded in persistent structural challenges. Concerns such as tightening margins, economic constraints, and unclear development plans (all at 69%) dominate sentiment, alongside geopolitical risks (51%) and ongoing issues around public sector effectiveness and crime (both 44%).

Yet, confidence—where it exists—is not without basis. Among the minority who are optimistic, 67% point to the suitability of government plans, while others highlight positive public sector signals (50%) and expectations of increased gas supply (39%). This suggests that confidence is closely tied to expectations of improved execution and coordination.

Policy Signals and Execution Gaps

The private sector is clear on where policy support is needed. Priorities such as encouraging foreign direct investment (58%) and digitalising government services (56%) stand out, alongside calls to strengthen manufacturing and exports (42%) and invest in agriculture (35%).

However, confidence in the Government’s broader economic blueprint remains mixed. Only 39% of respondents are optimistic about the Trinidad and Tobago Revitalisation Blueprint, with concerns driven largely by execution risks—particularly lack of clarity on funding (79%), limited confidence in government (76%), and bureaucratic constraints (66%).

At the same time, those who are optimistic see clear potential, with 78% believing the plan could drive diversification and investment, reinforcing the idea that the challenge lies less in vision and more in delivery.

Building Resilience Through Talent and Strategy

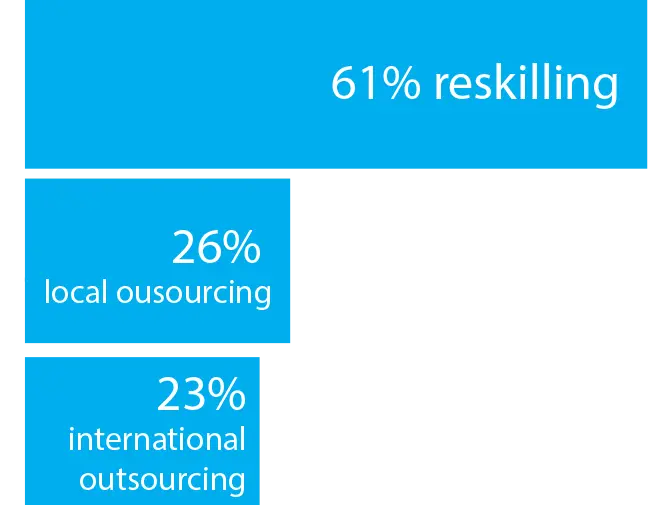

Organisations are responding to uncertainty by strengthening internal capabilities. A clear majority (61%) are focussed on reskilling and retooling existing employees, far outpacing other approaches such as outsourcing (26%) or sourcing talent internationally (23%).

This focus aligns with future skill needs, where digital capabilities (61%) and agility (54%) are seen as essential for competitiveness. Notably, workforce migration pressures appear contained, with 57% of firms reporting minimal movement (0–5%).

At the strategic level, disruption is expected to come primarily from emerging technologies, including AI (54%), as well as geopolitical developments (51%) and shifting customer expectations (49%). While most companies (79%) believe they are responding, they largely describe their approach as moderate rather than leading, suggesting room to accelerate execution.

Geopolitics and Foreign Exchange: Immediate Pressures

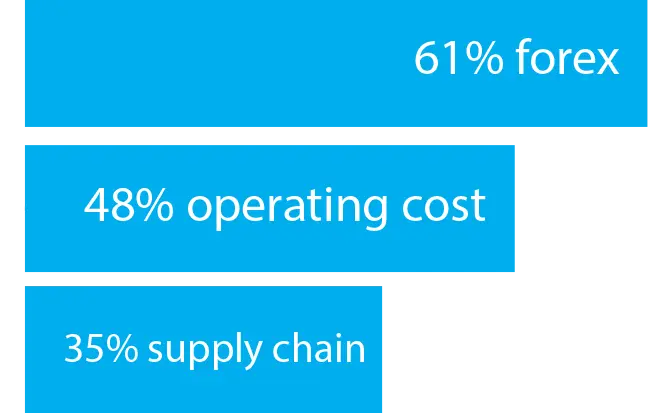

Geopolitical developments are no longer abstract risks—they are directly affecting operations. The most significant impact reported is difficulty accessing foreign exchange (61%), followed by increased operating costs (48%). In addition, 35% of firms report supply chain disruptions, while the same proportion say uncertainty is delaying investment decisions.

Foreign exchange challenges remain particularly acute. 70% of businesses rely heavily on forex, yet access has not improved—45% report no change, and another 45% say it has worsened. In response, companies are diversifying how they source foreign exchange, relying less exclusively on traditional banking (50%) and increasingly on alternatives such as export revenues (28%).

Despite these pressures, there is a degree of resilience in forward planning. 75% of organisations indicate plans to invest or expand in 2026, suggesting that businesses are choosing to move forward, even amid uncertainty.

Technology: From Adoption to Impact

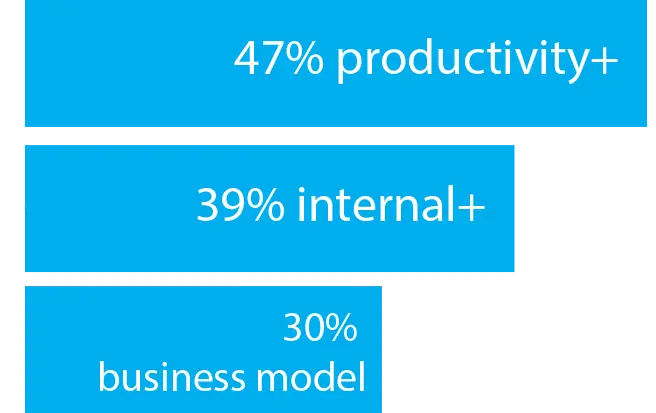

Generative AI is beginning to deliver tangible results. Nearly half of respondents (47%) report improvements in productivity and efficiency, while others highlight its impact on internal operations (39%) and business models (30%).

Looking ahead, expectations are even stronger, with 49% anticipating revenue growth and 44% expecting gains in innovation within the next one to two years. However, adoption remains uneven, with up to 21% indicating no investment or relevance, pointing to a widening gap between early adopters and those still on the sidelines.

Cybersecurity remains a parallel priority. Companies are focussing on resilience and recovery (44%), alongside cloud security (37%) and data privacy (32%). At the same time, barriers to adopting emerging technologies persist, particularly financial constraints (25%) and skills gaps (18%), reinforcing the need for both investment and capability development.

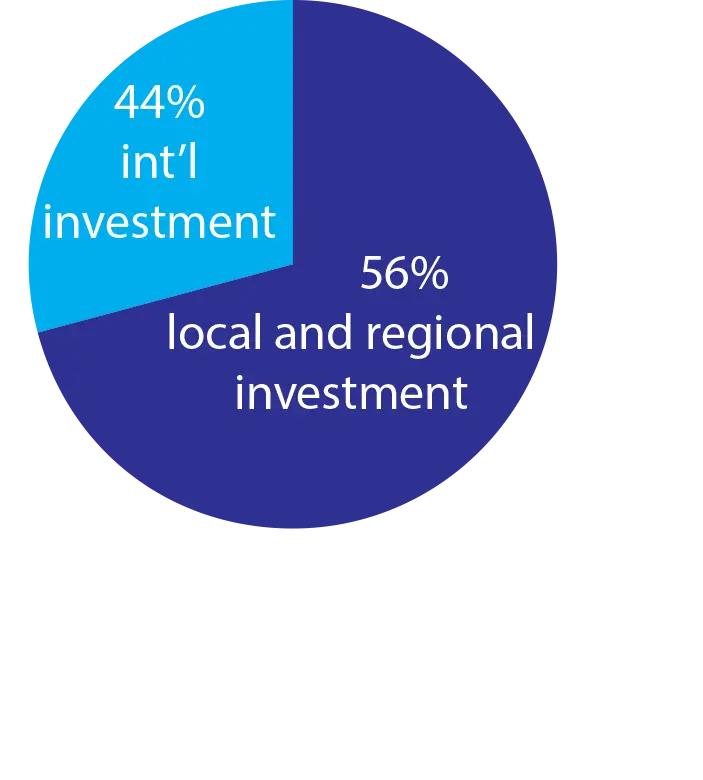

Investment and Operating Realities

Investment strategies are becoming more regionally focussed. While 44% of companies have deployed capital outside Trinidad and Tobago, most (56%) remain cautious. The Caribbean (40%) and Trinidad and Tobago (36%) are the top priorities, with limited interest in markets such as the United States (9%) or Latin America (10%).

At the operational level, safety and governance issues continue to shape the business environment. 11% of respondents report instances of bribery, while crime is driving increased costs for 53% of companies and contributing to client losses (11%) and reduced productivity (9%).

Turning Crosswinds into Opportunity

The data points to a business community that is not disengaged, but disciplined and pragmatic—clear about the risks, selective in its optimism, and deliberate in its response.

The defining question for 2026 is not whether disruption will continue, but how effectively organisations will respond. From managing geopolitical exposure and foreign exchange risk to and technology, the path forward will require sharper execution and stronger alignment between public and private sectors.

In a landscape defined by uncertainty, those that act with clarity and conviction will be best positioned to turn crosswinds into opportunity.